Introduction

Before the financial crisis of 2008/2009, neoliberalism had “enjoyed a global ideological hegemony unparalleled in modern times” (Ferguson 2012). This popularity of neoliberalism is certainly puzzling given that neoliberalism traditionally had been unpopular to the point that von Hayek questioned its compatibility with democracy (Hayek 1999). The sudden turn toward neoliberalism sometime in the mid-1970s is, thus, certainly in need of explanation. In his groundbreaking 2005 study “A brief history of neoliberalism” (Harvey 2011), Harvey explains that neoliberalism is both a utopian and political project. The former is based on neoliberalism’s seriousness toward ideals of human dignity and individual freedom. The latter refers to the elite form of economic class warfare implied in neoliberalism’s economic principles of free markets and low taxes among others. Harvey deems the latter to be the deciding factor influencing the turnaround of the mid-1970s, as that time saw steep declines of possessing classes’ relative economic advantages and thus confronted the privileged with a moment of crisis (Harvey 2011, p. 16). Harvey shares this view with, e.g., Wolfgang Streeck, who, in his perspective on a 1970s that turned out to be less late capitalist but early neoliberal, explains the unexpected rise of neoliberalism with an economic elite rediscovering its own paradigm only in a moment of crisis (Streeck 2013, p. 54). I do think, however, that even if one allows for the crises of the moderated postwar forms of capitalism to be a trigger of the neoliberal turn, it is somewhat unconvincing to assume that investors only represent their interests forcefully when in trouble. Rather, one could argue that after the early 1970s drop in asset values, capitalists had fewer resources and should have been confined to a more defensive lobbying for their special interests as a result. This, of course, is not what has happened, but it lends credence to the notion that we might want to be careful to subscribe fully to the class warfare explanation of the neoliberal turn. This leaves us with the ‘neoliberalism as a utopia’ hypothesis. From this perspective, “The Historic Roots of the Neoliberal Program” (Henry 2010) was an analysis of the condition(s) of totalitarian rule. The ordo liberals of the 1930s identify the idea of economic planning, policy intervention into free markets as it had developed after the economic depression of the 1870s, as the root cause of all forms of totalitarian politics, Nazism and Communism alike (for a classical account, see Eucken 1965). Interestingly, they emphasize the crash of 1873 with post-WWII thinkers such as Habermas and Arendt, whose prominence and importance in political theory circles took off in the 1970s. For Habermas, the 1870s depression marked the beginning of the entanglement of the public and private spheres (Habermas 2013, p. 225). Arendt traces her concept of imperialism to the economic difficulties of that era (Arendt 2011, p. 333). It could thus be argued that by the mid-1970s, neoliberalism’s normative positions vis-à-vis state interventions were more widely shared, facilitating its emerging dominance. This perspective fails to explain, however, why the decades immediately following the Second World War were so complacent toward the totalitarian risks of macroeconomic policy interventions. One might assume that political and economic theory discourse just needed time to recognize the centrality of the 1873 depression as a crossing of the abandoned path of liberalism and the fatal route toward totalitarianism. However, this argument, time, is double edged. It does not account for the largely positive—economically and democratically—experiences with the Keynesian economic policies of the 1950s and 1960s. There is, of course, then again a wealth of literature on the failings of Keynesian political economy (for a, once more, classical account see (Friedman 2016)), which, by the time of the 1970s stagflation, obviously was in trouble. The point for this paper, however, remains that Keynesianism had not led to totalitarian politics or an inevitable or long-lasting slowdown in economic growth. In contrast, the roughly three decades between the end of WWII and the mid-1970s saw higher economic growth and arguably greater intrasocietal, political emancipation than the following neoliberal era (Whalen 2021). When asking why neoliberalism became the dominant political economy of the West in the 1970s, one might thus assume that its real appeal was its (anti)ideological zeal delegitimizing communism as merely another form of totalitarianism. It is certainly supportive of this thesis that politicians such as Thatcher and Reagan were as much cold warriors as they were neoliberals. The question remains why the democratic West only embraced neoliberalism as its ideological weapon in the Cold War in the 1970s and not earlier. The paper at hand now assumes that this is because it is not so much classical neoliberalism that came to dominate the political economies of the West but financial neoliberalism . This term shall denote the American version of neoliberalism mainly based on option price theory . Once said theory was completed by the works of Black and Scholes (Black & Scholes 1973), it offered a seemingly scientifically proven and actionable calculus from which to translate economic problems into financial ones. Combined with the neoliberal conviction that self-regulating markets exist and offer the only way to determine fair prices (Fama 1970), option price theory provides the framework from which to argue for the marketization, financialization and privatization of hitherto regulated and public goods. Its argumentation is rigorous, principled and radical; thus, it can explain a sudden and decided political turn. Financial neoliberalism is based on the premise that there is a riskless return that “must be at the short term interest rate” (Black & Scholes, 1973, S. 643). I argue that this assumption of a riskless return at the bottom of the return matrix implies that, for all real short-term rates of greater than zero, money can create money by itself (Mix 2021). This, now, is a direct refutation of Marx. From this perspective, financial neoliberalism, once mathematically derived in the early 1970s, can be understood as a rejection of the central role of labor in societal reproduction functions and a very powerful new argument in the ideological struggle of the East/West divide. Fittingly, the greatest emancipatory achievement of the neoliberal era has been the Western triumph in the Cold War. Politically, with regard to the intrasocietal dynamics of Western democracies, it stands to reason that the now seemingly scientifically proven fact that modern financial markets have found the philosophers stone and can create wealth without work has different implications. First, capital’s newfound capacity to recreate itself is, obviously, a very convenient belief for everyone already with capital to employ. However, second, it is also a promise for everyone eager to prove him or herself in the newly energized fields of trading and investing. Third, it is a trap for neoliberalism’s remaining critics, as financial markets claim that they (re)distribute the wealth they ‘create’ along meritocratic principles. Thus, critique can be labeled resentment 1 . Finally, for this paper, it is also an angle because if we assume that financial neoliberalism is basically a function of options price theory and real rates, we should be able to time it precisely. This, now, is the aim of the present article.

When did neoliberalism end?

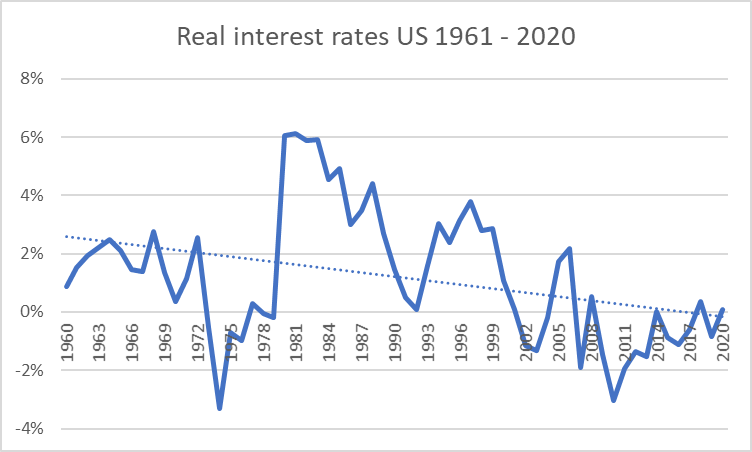

Neoliberalism ended when real interest rates (in the US and Western Europe) turned negative in approximately 2010. This hypothesis is based on the observation that ever since the completion of capital markets theory by Black and Scholes (Black & Scholes 1973), positive real interest rates imply an increasing share for capital of the national income (Mix 2021). Seen from this perspective, neoliberalism’s reign as a policy (that is, not just as another theory or worldview) lasted from 1981, when real rates turned sharply positive, to 2010, when they fell into the negative territory they still struggle to climb out of.

Figure 1: Real interest rates in the US from 1961-2020 (as percentages); Source: Federal Reserve Economic Data (FRED); Own computation

This paper is both a resumption and extension of prior writing about the interrelation between safe real rates, options price theory and neoliberalism. As such, it starts with the above hypothesis, which I will now research and scrutinize. However, first, some definitions and delimitations seem in order.

Following Hamilton et al., this paper defines real interest rates as “the nominal short-term policy rate minus expected inflation” (Hamilton et al. 2016, p. 4). This definition seems appropriate for the research interest of this paper, as Black and Scholes’ riskless interest also equals the short-term interest rate (Black & Scholes 1973). Another advantage of using this definition of real interest is that it provides a steady state value and thus opens the otherwise rather econometric field of interest rate theory for the political-economic perspective envisioned here. For this very reason, I also use the most straightforward calculus for real interest rates: the average short-term policy rate for the year minus the average rate of inflation for the same year. I know that it can reasonably be argued that this is an ex post calculus and that economic agents act on inflation expectations (Yi & Zhang 2016). I feel, however, that for the purposes of this paper, a comparison between actual numbers yields the most informative results, as I set out to investigate the consequences of certain moves in real interest rates for the everyday experience of the neoliberal political economy.

Neoliberalism as an unsustainable game

I argue that Black and Scholes’ assumption of an identity between the riskless return and short-term interest rates “shift [s] the expected returns of all risk assets upward as every rational investor would now demand a return in excess of the risk that he/she is carrying” (Mix 2021). As a result, capital share in national income grows as expected (and then realized) returns for all investments cumulatively yield more than the nominal growth rate (i.e., inflation and growth). This, however, is not a sustainable situation, as ‘a share in something’ cannot grow indefinitely and certainly cannot exceed 100%. For this good reason, prior liberal political economies had connected their concepts of risk and return in ways resulting in an equilibrium in which cumulative returns on equity equal the nominal growth rate. For this equilibrium to hold, it seems allowable, even necessary, that some risk investments overperform, i.e., with new industries rising while other old industries underperform or even recognize losses. This is creative destruction; capital flows from the latter to the former, actualizes the capital stock and decreases returns on it at the same time. What seems to disbalance this equilibrium, though, is a combination of the implications of option price theory and positive real rates because any real riskless return on capital has to be paid by someone else, i.e., labor. Imagine a game in which you are guaranteed a win. Even if it is a small win, it is, per definition, money from one of your fellow players to you. For this reason—guaranteed losses—it seems unlikely that one would find many fellow players for such a game if participation is optional. If, on the other hand, participation is mandatory and the player assigned the role of eternal loser has other income exceeding his guaranteed losses, the result of the game is an accumulation of wealth on the one hand and an accumulation of frustration on the other. This is now, I argue, what happened in the US after real rates turned positive in 1981 with dramatic consequences.

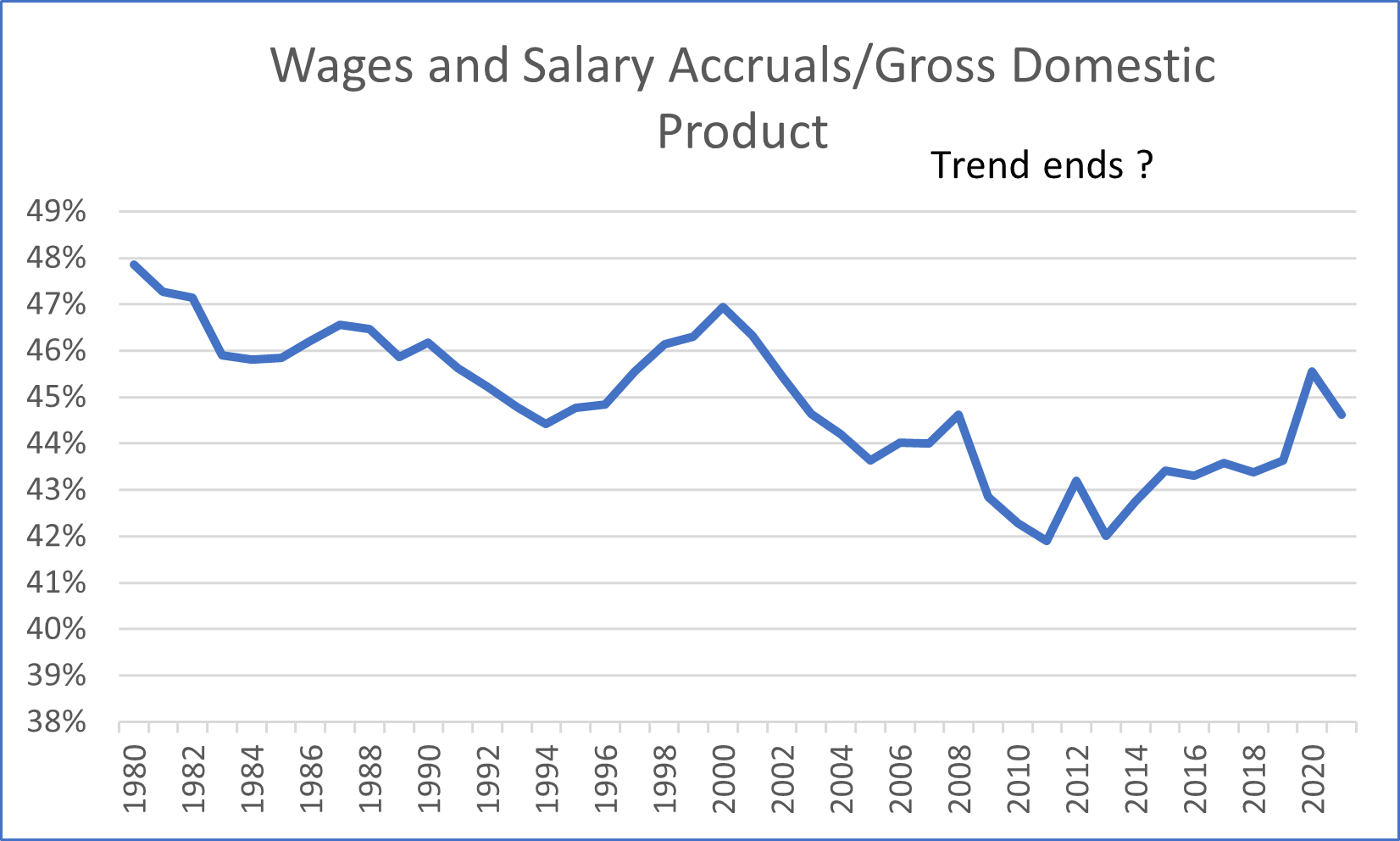

After a not-so-happy experiment with credit controls in early 1980, starting in November 1980, the Volcker Fed finally raised interest rates at a steeper rate than the increase in inflation (Mussa 1994; Schreft 1990). For the first time since the early 1970s, real rates turned positive in 1981 (see Figure 1). Somewhat as expected, the following recession of 1981-1982 fell mainly on the goods manufacturing industries (Sablik 2013). Goods were particularly hard hit, as consumers hitherto had, in anticipation of ever faster raising prices, gotten used to spending their incomes quickly. Now, positive real rates gave them an incentive to save again, reducing demand. The real surprise and, indeed, paradigm shift of the 1980s economic history thus became the following recovery. When, by the summer of 1982, the Federal Reserve began to gradually loosen monetary policy again, it was the resulting recovery that was transformational. It started with a stock market rally (Aug 1982) and only extended to the ‘real’ economy in late 1982/early 1983. In addition, when recovery finally came about, it was services heavy, meaning that the manufacturing jobs lost during the recession did not return but instead other jobs emerged in the service industries (Plunkert 1990). This change seems to be the primary reason for the most upsetting part of the 1980s expansion, that is, the slide of the labor share of national income even at times of economic expansion and productivity growth (Mishel et al. 2015). This shift has, of course, been duly studied. The main reasons given for the structural transformation of the American economy are a change in labor relations, globalization and increased automation (see., e.g., (Kochan et al. 1986; MacEwan 1996; Acemoglu und Restrepo 2021)). Importantly, these reasons are not mutually exclusive and likely all are true. It appears, for example, entirely possible that 1980s managers were looking for both automation and human resource practices aiming at nonunion business settings because international competition eroded their profit margins. None of the above reasons, however, seems to fully explain why, in a growing economy running at roughly full employment, as in say 1987, 1997, 2007, aggregate wages as a percentage of GDP fell in a more or less straight line.

Figure 2: Wages and salary accruals as a percentage of GDP (as percentages); Source: Federal Reserve Economic Data (FRED); Own computation

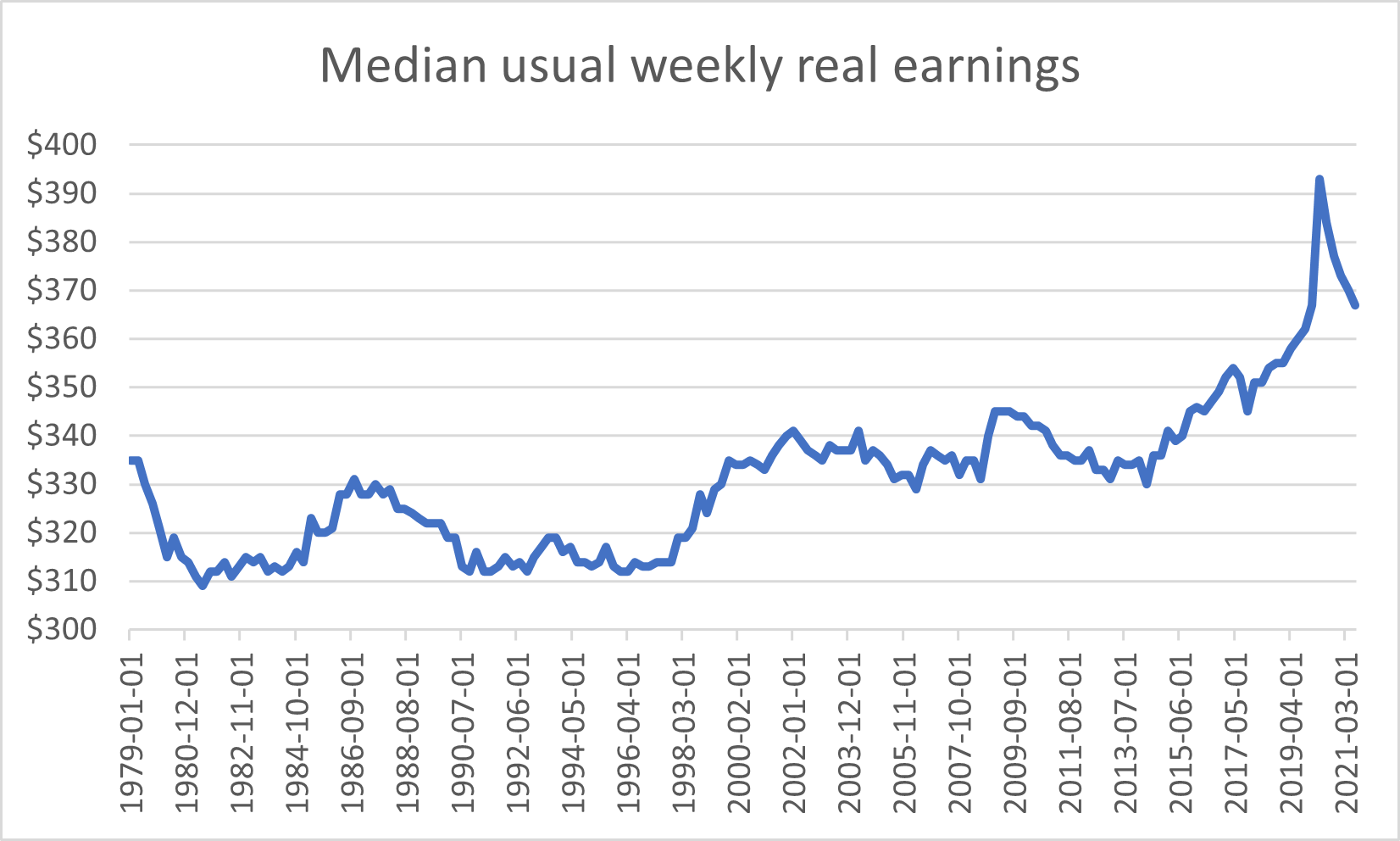

In other words, the above graph lends plausibility to the claim that Black and Scholes’ positive real rates seem to be the main drivers effecting a shift in income from labor to capital. This is because since real rates turned negative in approximately 2010 (see Figure 1; real rates were -1.9% in 2008, 0.5% in 2009, -1.5% in 2010 and -3.1% in 2011, i.e., they turned fully negative only in the 2010s), a turning of the trend seems observable. This phenomenon appears even more clearly visible in the (CPI adjusted) weekly real earnings of workers’ wages and salaries.

Figure 3: Median usual weekly real earnings, 1982-84 CPI Adjusted Dollars; Source: Federal Reserve Economic Data (FRED); Own computation

The above chart shows that US real wages and salaries were stagnant for the approximately 35 years from 1979 to 2014. Starting at USD 335 in the first quarter of 1979, real wages declined in the inflation and recessions of the early 1980s. They only fully recovered to USD 335 again in the fourth quarter of 1999 and hovered around that level for another 15 years. Since the fourth quarter of 2014 (USD 336), however, real wages have started to rise, first slowly and then, with pandemic relief funds in 2020, rapidly. With pandemic relief now largely a thing of the past once again, it will be most interesting to see where real wages develop from here. However, that is a discussion for another paper, possibly one on ‘ How neoliberalism did end.’ For now, it can be noted that the development of real wages supports the hypothesis of this paper, i.e., that the neoliberal era was founded on the interaction of real positive rates and options price theory and lasted from the early 1980s to approximately 2010.

Conclusion and future outlook

It is the hypothesis of this paper that neoliberalism as the hegemonic political economy was based on the interplay between rather arcane assumptions of options price theory and positive real rates. This combination yielded a political economy favoring capital over labor income to a point that it resembled an unsustainable game. Thus, it did not last but ended in approximately 2010. In other words, the hypothesis of this paper has been found to hold. It can now be stated in a pointed way that ‘neoliberalism ended when real interest rates turned negative in approximately 2010.’

Not the focus of this paper but a rather obvious desideratum are the political implications of the end of neoliberalism. Could it be that the political disorientation of roughly the last ten years is also an effect of an ideological vacuum more felt than understood hitherto?

References

Acemoglu, Daron; Restrepo, Pascual (2021): Tasks, Automation, and the Rise in US Wage Inequality. Cambridge, MA. Online verfügbar unter https://www.nber.org/papers/w28920, zuletzt geprüft am 23.02.2022.

Arendt, H. (2011): Elemente und Ursprünge totaler Herrschaft. Antisemitismus, Imperialismus, Totalitarismus. München: Piper.

Black, Fischer; Scholes, Myron (1973): The pricing of options and corporate liabilities. In: Journal of political economy 81 (3), S. 637–654.

Eucken, W. (1965). Die Grundlagen der Nationalökonomie. Berlin (West): Springer.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. In: The Journal of Finance 25, 383–417.

Friedman, Milton (2016): A Theory Of The Consumption Function. San Francisco: Golden Springs Publishing.

Habermas, J. (2013): Strukturwandel der Öffentlichkeit. Untersuchungen zu einer Kategorie der bürgerlichen Gesellschaft. Frankfurt am Main: Suhrkamp.

Hamilton, James D.; Harris, Ethan Schlozer; Hatzius, Jan; West, Kenneth D. (2016): The equilibrium real funds rate - Past, present, and future. IMF economic review. DOI: 10.1057/s41308-016-0015-z

Harvey, David (2011): A brief history of neoliberalism. 1. publ. in paperback, reprint. (twice). Oxford: Oxford Univ. Press.

Hayek, Friedrich A. von (1999): The road to serfdom. 50. anniversary ed., [Nachdr.]. Chicago: Univ. of Chicago Press.

Henry, John F. (2010): The Historic Roots of the Neoliberal Program. In: Journal of Economic Issues 44 (2), S. 543–550. DOI: 10.2753/JEI0021-3624440227.

Kochan, Thomas A.; Katz, Harry Charles; MacKersie, Robert B. (1986): The transformation of American industrial relations. New York: Basic Books.

MacEwan, Arthur (1996): Globalization and Stagnation. In: Social Justice Vol. 23 (No. 1/2), S. 49–62. Online: http://www.jstor.org/stable/29766925 , last checked 6. May 2022.

Mishel, L.; Gould, E.; Bivens, J. (2015): Wage Stagnation in Nine Charts. Economic Policy Institute. Online: https://www.epi.org/publication/charting-wage-stagnation/ , last checked 6. May 2022.

Mix, Andreas (2021): Is zero the safe real rate? In: American Review of Political Economy 16 (2). DOI: 10.38024/arpe.217.

Mussa, Michael (1994): U.S. Monetary Policy in the 1980s. American Economic Policy in the 1980s. Hg. v. Martin Feldstein. Chicago: University of Chicago Press. Online: https://www.nber.org/system/files/chapters/c7753/c7753.pdf , last checked 6. May 2022.

Plunkert, Lois M. (1990): The 1980's: a decade of job growth and industry shifts. In: Monthly labor review. Online: https://www.bls.gov/opub/mlr/1990/09/Art1full.pdf , last checked 6. May 2022.

Sablik, Tim (2013): Recession of 1981–82. July 1981–November 1982. Hg. v. Federal Reserve History. Federal Reserve Bank. Online: https://www.federalreservehistory.org/essays/recession-of-1981-82 , last checked 6. May 2022.

Schreft, Stacey L. (1990): Credit Controls: 1980. In: FRB Richmond Economic Review vol. 76 (No. 6), S. 25–55. Online: https://ssrn.com/abstract=2122688, last checked 6. May 2022.

Streeck, W. (2013). Gekaufte Zeit. Die vertagte Krise des demokratischen Kapitalismus. Berlin: Suhrkamp.

Whalen, Charles J. (2021): Post-Keynesian Institutionalism and the Failure of Neoliberalism: Returning Realism to Economics by Highlighting Economic Insecurity as the Flip Side of Financialization. In: Journal of Economic Issues 55 (2), S. 469–476. DOI: 10.1080/00213624.2021.1909346.

Yi, Kei-Mi; Zhang, Jing (2016): Real Interest Rates over the Long Run. Decline and convergence since the 1980s, due significantly to factors causing lower investment demand. Hg. v. Economic Policy Papers. Federal Reserve Bank of Minneapolis. Online: https://www.minneapolisfed.org/article/2016/real-interest-rates-over-the-long-run , last checked 6. May 2022.

-

From the perspective developed here, this dynamic of ascription, subjectivation and exclusion of ‘failure’ under neoliberal conditions is almost certainly a driver of the authoritarian populism challenging liberal democracy. It is, however, not the topic of this paper, which rather deals with a potential ‘light’ at the end of the neoliberal tunnel. ↩︎